What’s driving accelerating social inflation?

Swiss Re on ‘shocking’ figures around corporate trust

At Swiss Re’s latest sigma market briefing at RVS in Monte Carlo, the message to the re/insurance industry was clear – liability claims costs are rising faster than the rate of economic inflation in several major economies, and they’re showing no signs of abating. It’s a trend being thrown into sharp relief amid a solid global growth outlook, with economic disinflation to 2% being on course in Europe for 2024, and in the US for 2025.

In a Press briefing on the report, senior leaders from the reinsurance giant revealed how it has constructed a “social inflation index” in order to disentangle it from other claims drivers. On this basis, Swiss Re estimated that social inflation drove around 7% of the claims growth in US liability insurance in 2023. Putting those two key figures – 2 and 7 together – Jerome Haegeli (pictured), group chief economist at Swiss Re noted that you get 27 – the number of court cases awarding more than $100 million in compensation against commercial defendants last year.

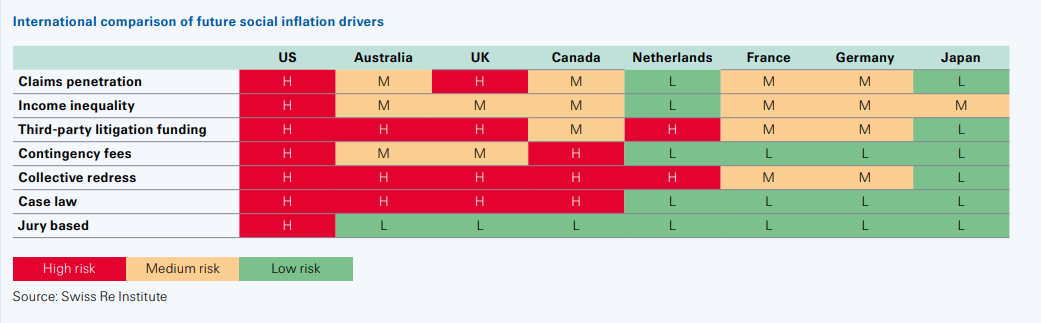

What are the key drivers behind future social inflation?

With social inflation creating underwriting losses and adverse reserve development, it’s clear that insurance rate increases have not compensated for rising loss costs, delivering cumulative underwriting losses of US$43 billion between 2019 and 2023. With social inflation set to stay in the US and increase in Europe, it’s critical to understand the key drivers behind future social inflation.

These drivers have been identified as:

- Claims penetration

- Income inequality

- Third-party litigation funding

- Contingency fees

- Collective redress

- Case law

- Jury based

The graph below offers an international comparison of these future social inflation drivers:

Haegeli noted that this wave of social inflation is the third spike seen since the phrase was coined in the 1970s. While this latest cycle might not yet be hitting the highs it has in the past, it differs from previous cycles for a few key reasons, the first being that the length of the cycle being seen is long compared to previous iterations. In addition, there’s no sign of social inflation abating, as the key factors driving it – including litigation funding, US court verdicts and distrust in corporations, continues to accelerate.

Digging into public trust in institutions

Distrust in corporations was identified as a key concern by the sigma report, which outlined that public trust in institutions is declining across many of society’s institutions. This is illustrated in a survey carried out by Swiss Re last year which found that 82% of respondents believed the damages awarded in lawsuits are “just right” or “too low”. Another survey found a near doubling of anti-corporate sentiment from 27% pre-pandemic to 45% post-pandemic.

To further compound matters, 77% of jurors believe in the use of punitive damages to “punish a corporation”. Citing a 2023 behavioral economics survey in an interview with Re-Insurance Business, Haegeli underscored income inequality as a key driver of this trend. “Forty-four per cent [of respondents] say firms should pay medical compensation even if not responsible for an accident, that’s in the US.

“An example is that if you fall or slip in the mall, it may be as a result of bad shoes or maybe you just fall, but these respondents believe that the shopping mall owners should still pay. With income inequality in the US being higher than in Europe, we see this as one of the limiting factors in why, while social inflation is on an upward trend in Europe, it will not be the same as seen in the US because you have social welfare, security and protection in Europe.”

The research’s findings around corporate trust are really shocking, he said, with 87% of those surveyed saying that they believe large companies prioritize profit over safety. It’s inbuilt into the business model of corporates to attempt to maximize shareholder value, but if it’s done at the expense of safety, then something has gone wrong. “Rising income inequality as well as litigation habits and litigation financing and legal systems are all ingredients in a cocktail which, when you put everything in together, makes for a bad outcome.”

The unsocial implications of social inflation

What’s critical to bear in mind, Haegeli said, is that the consequences of this are incurred not just by insurance companies but by society at large. In Warren Buffet’s letter to Berkshire Hathaway’s shareholders in 1997 – in the first public instance of the phrase being used – he emphasized the need to increase insurance rates due to the ‘social inflation’ of changing attitudes to suing and being sued. “It’s called social inflation but there’s nothing social about it at all when the costs are going to be borne by society.”

What can be done to mitigate the impact of social inflation?

As to what can be done to build greater trust in corporations and, more broadly, to fight against rising social inflation, Haegeli said that, at the end of the day, as an economist, he’s a big believer in the power of transparency and having free market prices. Having transparency means having a greater understanding of who’s financing third-party litigation funders, and how the profits from these awards are being distributed.

“That will go a long way in alleviating the problem,” he said. “And it’s not about changing the legal system, it’s about making sure that it works for everyone. The plumbing of the legal system can only work well if you know where the flow of funds is really coming from and where it’s going. In some cases in the US, you have foreign funds financing hedge funds and the payout being disproportionate to the hedge fund. If that was more widely known, I have no doubt that the outcome would be different.”

Related Stories

Keep up with the latest news and events

Join our mailing list, it’s free!